February Signals: A Bigger Music Industry, and a More Exposed One

By the time March arrived, February had already left a clear set of fingerprints across the music industry in the UK, Ireland and Europe. It was a month that celebrated scale, spectacle and global reach. It was also a month that quietly exposed the fragile economics underneath the whole enterprise.

Music has always lived inside that contradiction. February simply reminded everyone again.

The clearest symbolic moment came in Britain, where the Brit Awards moved to Manchester for the first time in their history, landing at Co-op Live on 28 February. After nearly five decades in London, the relocation was framed as a recognition of Manchester’s deep musical legacy and its contribution to British culture. For a city that produced Joy Division, The Smiths, Oasis and The Stone Roses, the symbolism was obvious enough. The centre of gravity for British music has never belonged exclusively to London, even if the industry sometimes behaves as if it does.

On the night itself, Olivia Dean emerged as the ceremony’s dominant winner, taking four major awards including Artist of the Year and Album of the Year. The sweep reinforced a broader shift within British pop toward artists who move fluidly between soul, pop and alternative traditions rather than sitting inside rigid genre categories. The BRITs themselves confirmed the results shortly after the ceremony, with coverage widely reported across British media.

The ceremony also reflected the increasingly global shape of the music industry. For the first time in its history the BRIT broadcast featured a K-pop performance. Rather than a traditional idol group appearance, the segment featured EJAE, Audrey Nuna and REI AMI, performing the track “Golden” as the singing voices of fictional group HUNTR/X from the Netflix animated series KPop Demon Hunters. The performance was filmed in Manchester and aired as part of the live broadcast, signalling the extent to which Korean pop culture has become embedded in global music entertainment.

Awards nights are theatre, though, and February made it clear that the real story of the music industry rarely sits on the awards stage. It sits underneath it.

The Music Venue Trust spent much of the month continuing to highlight the findings of its Annual Report 2025. The report painted a stark picture of the grassroots touring ecosystem in Britain. According to the organisation’s research, 53 percent of UK grassroots music venues made no profit in 2025, with average profit margins sitting around 2.5 percent. The venues collectively contributed more than £500 million annually to the UK economy, yet many remained financially precarious.

These venues are not decorative parts of the music ecosystem. They are where artists develop their craft, test new material and build their first audiences. When more than half of them cannot turn a profit, the industry is not merely facing a temporary squeeze. It is facing a structural imbalance between cultural production and financial sustainability.

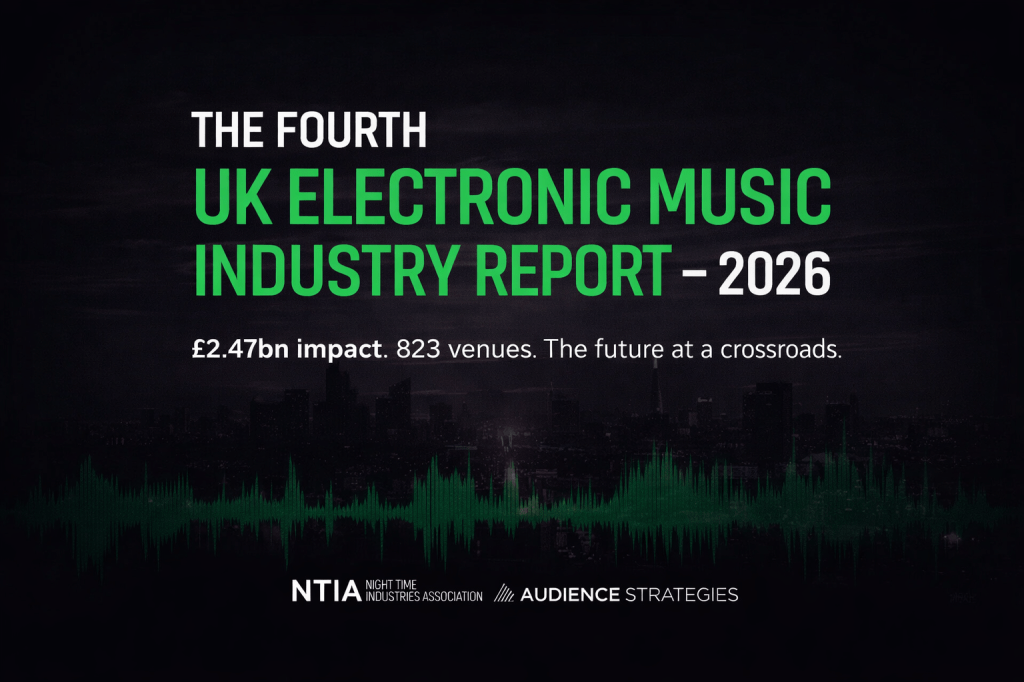

February also brought sobering figures from the Night Time Industries Association, which published its Fourth UK Electronic Music Industry Report. The report estimated that the UK electronic music sector generated £2.47 billion in economic activity in 2025, yet the number of operating nightclubs had fallen to 823 venues, representing a 36 percent decline since March 2020. Event programming had increased by more than 10 percent year on year, highlighting a strange contradiction: audiences continued to seek out live music experiences even as the physical infrastructure supporting those experiences continued to shrink.

One phrase from the report captured the problem neatly. The sector was suffering from a “missing middle”. Mid-tier venues, the stepping stones between grassroots clubs and large arenas, now represent only a small portion of the live infrastructure. Careers in music rarely leap from 150-capacity rooms to arena tours overnight. They need ladders. February offered a reminder that many of those ladders are losing rungs.

Across the Irish Sea, February’s most significant industry signals came from policy rather than spectacle. During a hearing of the Joint Committee on Arts, Media, Communications, Culture and Sport in the Oireachtas, Victor Finn of the Irish Music Rights Organisation outlined the scale of Ireland’s music economy.

The figures were impressive on paper. Music contributes roughly €1 billion annually to the Irish economy, directly supports around 13,400 jobs, and surveys show 71 percent of Irish adults consider music important in their daily lives. But the same testimony also revealed a more uncomfortable truth. The average net income for people working in music was approximately €15,530, and nearly 70 percent of music professionals required additional employment to sustain themselves.

Ireland celebrates music as part of its national identity. February’s evidence session suggested the country still has work to do when it comes to paying the people who produce it.

The hearing also touched on one of the most contentious topics currently facing the global music industry: artificial intelligence. Finn warned that rapid developments in AI systems pose significant risks to creators if copyright protections and remuneration frameworks are not properly enforced. He pointed to Ireland’s proposed AI regulation legislation and wider EU discussions around transparency and compensation when copyrighted works are used to train generative models.

February also saw the final payments made under Ireland’s Basic Income for the Arts pilot scheme, which since 2022 provided 2,000 artists with €325 per week. The programme, widely studied across Europe as a cultural policy experiment, is now expected to transition into a longer-term model. While critics have questioned the limited number of places and the rotation of cohorts, the scheme nonetheless represents one of the few attempts by a government to stabilise creative work in an industry where income remains notoriously volatile.

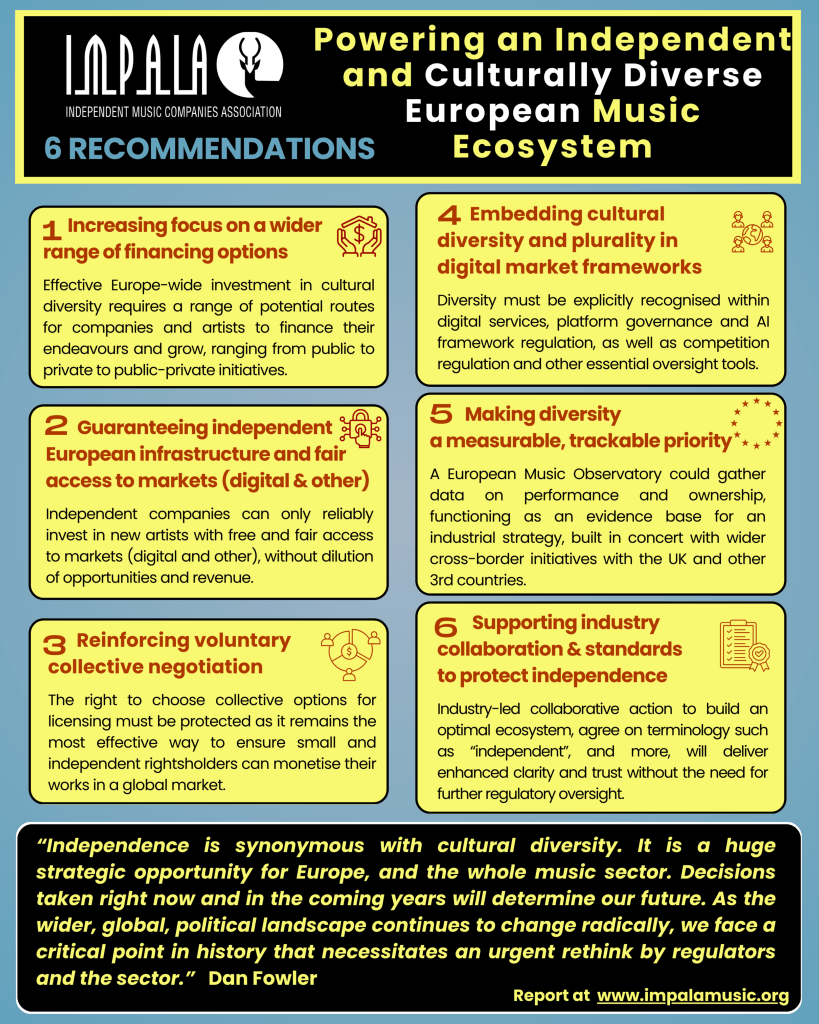

Across Europe more broadly, February’s industry conversations were shaped by structural questions about ownership and market access. The independent music association IMPALA released a report titled Powering an Independent and Culturally Diverse European Music Ecosystem. The report argued that Europe’s music sector contributes tens of billions of euros in economic value while supporting millions of jobs across the continent.

But the document also warned about the growing concentration of power within the digital marketplace. Recommendation algorithms, platform dominance and uneven access to market data were all identified as potential threats to cultural diversity in European music. When a small number of platforms control the mechanisms through which audiences discover music, questions about visibility and fairness become questions about regulation.

Digital platforms continued to loom over the conversation throughout the month. According to figures published in early 2026 by TikTok, research commissioned by the company suggested the platform generated approximately €1.8 billion in additional revenue for the European music industry in 2025 through streaming, live performance demand and merchandise sales. Even allowing for the usual caveats around corporate research, the broader point was difficult to ignore. Algorithmic discovery systems now sit at the centre of the music economy.

Thirty years ago radio programmers and record shops determined what audiences heard. Today, increasingly, recommendation engines do.

Looking back from early March, February did not produce a single defining headline. Instead it revealed a pattern and we must always look at patterns, for they tell a wider story.

The UK music industry demonstrated its capacity for spectacle while its grassroots infrastructure remained fragile. Ireland confirmed the cultural and economic value of music while many of its workers continued to earn modest incomes. Europe celebrated a diverse musical ecosystem while confronting the growing power of digital platforms.

The music kept moving. The crowds kept showing up.

The structural questions moved alongside them. We wilo be back next month to see how March pans out!

Leave a comment