New data from the European Audiovisual Observatory offers a fairly unvarnished view of where cinema sits across Europe right now, and it does not support the idea of a clean post-pandemic recovery.

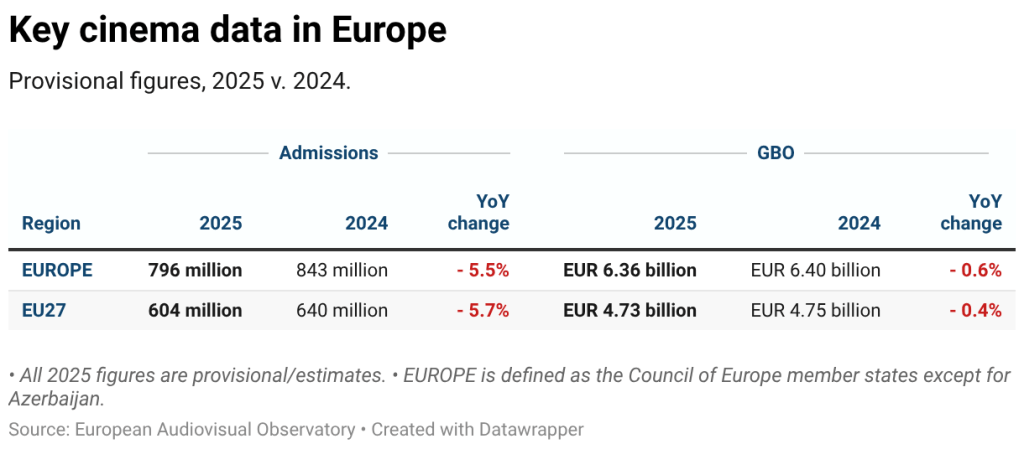

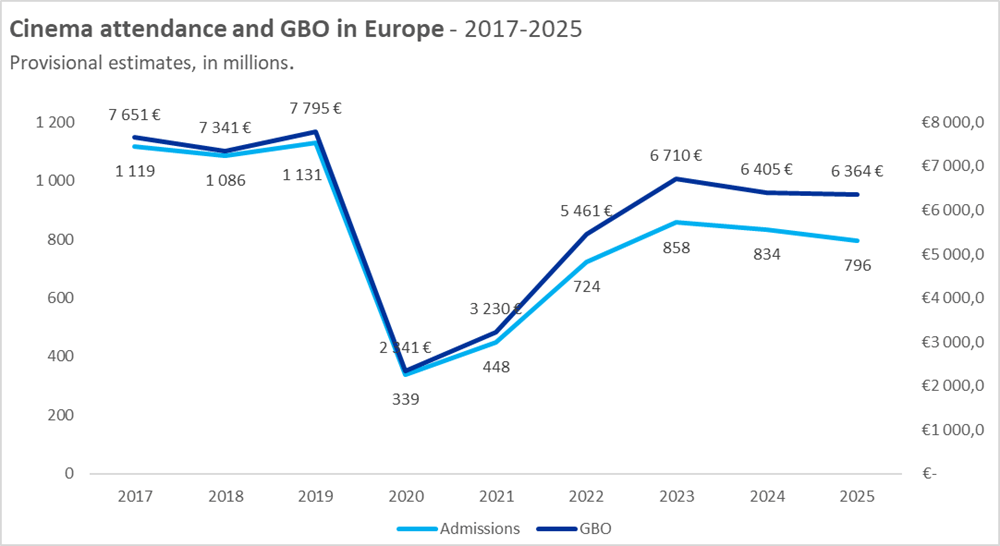

Cinema admissions fell by 5.5% in 2025, declining from 843 million to 796 million. That drop tells its own story, but what sits alongside it is just as revealing. Box office revenues remained comparatively stable, reaching an estimated €6.36 billion, only marginally down on €6.40 billion in 2024.

That stability is not driven by audience demand. It is being sustained by price. Average ticket prices rose from €7.6 to approximately €8.1, offsetting much of the decline in attendance and masking what is, in effect, a contraction in audience participation.

Admissions reflect actual behaviour, not yield.

To understand whether this is simply decline or something more structural, it helps to look at markets that are holding their ground.

France is the most useful reference point. Data from Vertigo Research places France at 2.3 admissions per capita in 2025, the highest in Europe, but the more revealing layer is demographic.

Audiences aged 15–24 in France average around 3.5 visits per year, with Italy showing a similar pattern at approximately 2.5 for the same cohort, while Belgium sees its strongest engagement among children. These outcomes point to markets where audience development is being treated as an active, ongoing strategy rather than a passive outcome.

The data point that deserves far more attention, however, sits with older audiences.

In France, those aged 60 and over attend cinema at an average rate of 1.5 times per year. That is not a disengaged cohort. It is a stable and consistent one.

What Does This Look Like in Ireland?

Ireland follows the same trajectory. Admissions dropped to 10.7 million, bringing per capita attendance to just over 2 visits per person annually. Not long ago, Ireland consistently sat among the strongest cinema-going markets in Europe, frequently exceeding 3 admissions per capita, so this is not a marginal fluctuation. It signals a meaningful shift in how audiences are engaging with cinema.

The implications of this become far more concrete when you look at the demographic reality. Approximately 30–35% of the population is now aged 55 and over, based on national data from bodies such as Central Statistics Office, and this is not a marginal audience segment. It is a substantial, financially stable cohort that grew up with cinema as a central and habitual part of cultural life.

This is the generation that sustained cinema-going long before streaming, long before algorithm-driven discovery, and long before the fragmentation of attention became the industry’s default explanation for decline. Their relationship with cinema is not theoretical. It is embedded.

And yet, across programming, scheduling and marketing strategies, they are rarely treated as a primary audience.

Instead, the dominant focus continues to sit with younger demographics, discovery culture and opening weekend performance, as though growth can only come from chasing new audiences rather than re-engaging existing ones. That is not just a strategic oversight. It is a misreading of where value still sits within the market.

Because when admissions fall from over 3 visits per capita to just over 2, as they have in Ireland, that is not simply about younger audiences attending less. It reflects a broader disengagement across the market, including audiences that historically formed the backbone of cinema attendance.

Particularly when the barriers to re-engagement are not complex. They are practical. Screening times that align with lifestyle, environments that feel accessible and welcoming, and programming that reflects audience interest rather than assumption. None of this requires reinvention. It requires attention.

What is missing in the Irish context is not demand. It is deliberate strategy.

At that point, the question becomes unavoidable. If admissions are falling, why is one of the most reliable and financially stable audience groups not being actively prioritised?

Ireland’s audiovisual sector is not a marginal cultural space. It is a significant economic engine, supporting close to 16,000 jobs and generating over €1 billion in annual economic impact, according to analysis commissioned by Fís Éireann/Screen Ireland. Cinema exhibition sits within that wider ecosystem, alongside broadcast and streaming, all competing for the same audience attention.

At the same time, that same research points clearly to a shift in audience behaviour, with traditional cinema and television increasingly under pressure from video-on-demand platforms and changing consumption habits. In other words, this is not simply a story of decline. It is a structural rebalancing of how audiences engage with screen content.

And yet, despite the scale of the sector and the clarity of these shifts, much of the strategic focus continues to sit on production, skills and international competitiveness, rather than on sustained audience development within Ireland itself.

What is happening across Europe suggests not disappearance, but misalignment.

Around two-thirds of European countries recorded declines in admissions in 2025, although the scale of those declines varied. Three markets alone accounted for the majority of the drop: France (-24 million admissions, representing nearly half of the total European decline), Spain (-8 million), and Türkiye (-5 million). Gains in other territories, including Germany, Poland and Austria, were not sufficient to offset these losses.

Despite this, France remains the largest cinema market in Europe with 156 million admissions, followed by the United Kingdom at 123 million and Germany at 91 million.

Part of the downturn has been attributed to a weaker year for US studio output and the absence of pan-European breakout titles, although American productions still dominate overall box office rankings. Titles such as Zootopia 2, Avatar: Fire and Ashes, Minecraft, Lilo & Stitch and Mufasa were among the highest-grossing releases across the region.

At the same time, several European markets saw strong performances from local productions. Films such as Das Kanu des Manitu in Germany, Černák in Slovakia, Buen Camino in Italy, Stelios in Greece and Yan Yana in Türkiye topped national charts, contributing to rising domestic market share in multiple territories, including Poland, Italy and Germany.

For exhibitors and distributors, this is not a theoretical problem. It is operational. Screening times, venue environments, pricing structures and community outreach all shape whether audiences feel invited or excluded. There is a persistent tendency to over-index on younger audiences and discovery culture while under-investing in audiences that already have an established relationship with cinema.

There is also a more straightforward step that is often overlooked. Ask the audience directly. Engage with retirement groups, Men’s Sheds, active age networks and local organisations. Understand what would make the experience more appealing or accessible. The insight gained from that process is far more valuable than assumption-led programming, and the act of engagement itself becomes part of the strategy.

Much of the current discourse around cinema continues to centre on decline, streaming competition and shrinking attention spans. Far less attention is paid to the audiences that remain both willing and able to attend but are not being meaningfully engaged.

That gap between audience potential and industry focus is where the real issue sits, and it is particularly pronounced in the Irish market.

Leave a comment